![]()

This article on the liberalization of Romania’s electricity sector originally appeared on Bilten.org in April 2018. We’re reprinting the English version of the text here.

On 1 January 2018, the Romanian electricity market was entirely liberalized. This has been a long process that started in 1998 with the formation of a national authority for regulating the electricity sector and was followed up with the break-up of the former communist integrated system into several companies in 2000. The liberalization, it was hoped and promised, will bring better services, real options for customers and smaller tariffs. After two decades the opposite is the case: producers and distributors act monopolistically and the prices have skyrocketed. This is yet another sad story of the post-communist transition.

In the third quarter of 2017 the price of electricity in Romania reached unprecedented levels. According to DG Energy, a structure of the European Commission, the median price for electricity in Romania was the highest in the EU, a 52% increase compared to 2016, whereas in the rest of the EU the increase was only of 7%. This is unfathomable since the proportion of the energy produced based on fossil (which is more expensive) is lower in Romania compared to many other European countries. One of the reasons invoked was a decrease in the production of electricity from water and fossil due to objective factors. In fact, as many voices complained, it all smacked of a clear price fixing scheme between the two largest producers of electricity. By lowering production they were able to increase prices knowing full well that the national authority in charge of regulating the energy sector (ANRE in the Romanian acronym) will not be willing, or able, to intervene in the context of a deregulated market. The Competition Council, a state agency in charge with overseeing trading, promised to take a look into the matter but it never actually did. A special Parliamentary commission was set up to investigate the matter but its report was immediately classified without being presented to the public.

Unsurprisingly, when energy companies published their balance sheets in early February 2018 their profits were substantial. Most staggering, Romgaz, one of the top two gas producers in Romania recorded a 38% income increase from electricity production compared to 2016, and a 15% increase of electricity production. Hidroelectrica, the main electricity producer, reported a 16% profit. A few weeks ago the company was embroiled in a public outcry when it was reported that the management of the public-owned company plans to double the salaries of its directors (already astronomic compared to the average state salaries) precisely as a result of its positive balance sheet in the previous year. In fact, such an increase is legally stipulated by a previous Governmental Decree that will come into force in the fall.

The distribution companies were affected by the rising costs, albeit they too registered a profit. The real losers were the final consumers, especially the about 8 million registered households, that by October 2017 saw their bills increased by 8% to 9,5%, depending on region. They are the ones set to lose in the long term as well, as it will be described further.

One of the effects of liberalization is that individual consumers (that is households) can now directly chose an electricity provider based on the best available offer in their region. However, according to existing data from ANRE, only 1 in 8 consumers did so, and only a fraction of those who did, chose a different provider than the established ones. The rest are still relying on the previous big 4 providing companies, which are now functioning in a different regime than in the free market system: that is, the last-gasp provider, hence prices are significantly higher than in the free market system. What appeared to be a blessing for consumers who would be able to freely choose their own providers and thus lower the costs while encouraging competition, in effect only strengthened the power of the big players. And this is the whole paradox: the much-vaunted liberalization of the energy sector only strengthened monopoly companies. Their profits went up together with the consumption bills.

As everywhere else, the post-communist restructuring of the energy sector in Romania sought to replace the previous state monopoly with a free market for energy, turning energy consumers into customers. More specifically this meant breaking down the system into various interconnected but independent actors: producers, transporters, distributors, providers and customers. The aforementioned ANRE functions as an oversight mechanism with limited powers to control. Energy is bought and sold on the electricity bourse (OPCOM, the Romanian acronym). The electricity production is dominated by a handful of major players. Hidroelectrica, a fully state-owned company, is the biggest producer of electricity in the country with over 42% of the total. The profits go to the state budget (being subordinated to the Ministry of Economy), but there are plans to list about 10% of the shares to the stock exchange starting this year. The state therefore has a vested interest in making this company profitable, but this has been the case only recently. In the past half a decade the company was in insolvency, due to a mixture of bad management and syphoning of funds. Some analysts intimated that the price hikes in late 2017, of which Hidroelectrica was the main beneficiary, was an attempt to shore up the company in order to speed up its listing. Nuclearelectrica, also entirely state owned, is the second biggest producer of electricity, accounting for about 20% of the total. Coal (state owned) and gas (foreign owned) electricity production account for 10% each.

On 11 April 2018, for the first time, the solar energy production was higher than the one produced by one of the nuclear reactors. Largely related to uncharacteristic warm and sunny days in 2018, the solar energy production accounts now for between 10%-15% of the total. However, this sector, albeit lacking the monopolistic character of the big two, is also contributing to increasing the electricity bills of final customers, as I will explain below.

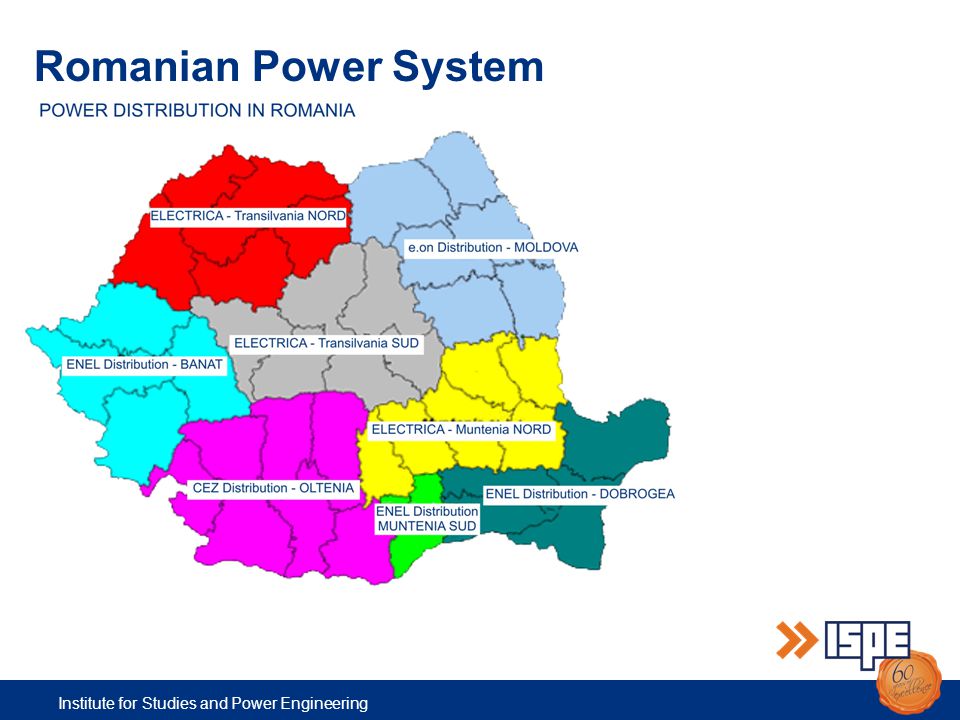

In terms of transportation and distribution, monopoly is also the rule. Transelectrica is the sole, state-owned, company that transports the energy from producers to distributors. Electrica (a private company but with the Romanian state a majority shareholder), ENEL (Italian), CEZ (Czech) and E.On (German) are the four electricity distributors that cover monopolistically the entire territory of the country, divided in 8 regions. ENEL and Electrica are the biggest players, covering more regions and the wealthier ones at that. However, despite the price increase, they also reported significant rates of profit in 2017. What is more, as stipulated by the privatizing contracts, distribution companies can deduct their investment in modernization of the infrastructure by including the costs into the final bills paid by consumers. There were numerous cases in the past years that this practice was abused in order to increase profits and cover loses. E.On for example was exposed for doubling the bills for both gas and electricity. In 2012, the heads of ANRE and ENEL were put to trial in a corruption case. Customers were charged the green tax twice (see below) but the two entities agreed to refund only a small portion of the funds, the rest staying in ENEL’s accounts. This was the most notorious such instance, but the practice was widespread among all distributors.

These structural advantages basically divide the market into four undisputed monopolies. Hence liberalization had a very limited effect. In fact, these four monopoly players have no incentive to push consumers into the free market (where the price is lower) and have all the reason to keep them in the last-gasp market where prices are regulated but higher. Albeit ENEL and E.On flexed their muscles in the free market (where they managed to double their share at the expense of Electrica), this market remains too miniscule to be relevant (0,85 TWh, compared to 26 TWh). Hence they will be able to continue to impose a fixed price agreed with ANRE to their own advantage.

A new law that is being debated in Parliament at the time of the writing will further increase the already mentioned trends: monopolization and price increases. The bill stipulates that the distributors are obliged to buy the so-called “green certificates” (the EU-wide renewable energy supportscheme) until 2022. This is part of the local efforts to meet the obligation of 24% energy production from renewable sources agreed with the EU. This scheme was criticized on two accounts. First, it represents a direct subsidy of green energy production by consumers. Solar- and hidro- energy producers will stand to benefit the most. Secondly, the 24% target assumed by Romania is not only unrealistic but also above the EU requirements of 20% (Poland negotiated 15% given its dependency on fossil). Since buying these certificates is mandatory (and the price necessarily incurred by consumers) it leads to the formation of a profitable market in which only a few established actors will stand to benefit. The planned increase is not unsubstantial either: from 11,7 euro/MWh in 2018 to 14,5 MWh in 2022.

Romania will thus become the poorest country with the highest electricity bill in the EU. Whether this is the failure, or precisely the success, of liberalism in post-communism, it is perhaps irrelevant. We need to turn off the lights anyway.